Daily Insights Report 14/02/17

- 31 Mar 2017

14 Feb 2017

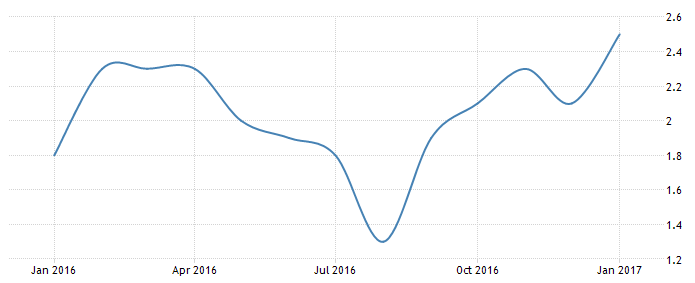

Data released yesterday from China showed that inflation was 2.5% year-over-year in January. This is an increase of 0.4% from December, when inflation was 2.1%. This has been the highest level of inflation seen in China’s economy since May 2014. The graph below shows how inflation has moved in the past year.

The Australian Dollar strengthened 0.4%. This comes after the business conditions showed to jump in January as a survey conducted by National Australia Bank showed. This survey’s data has been so positive since 2011.

Euro (EUR)

Italy: GDP (December)

It is likely that Italy’s economy continued to grow in the final quarter of 2016. The second last quarter of last year showed the economy to be growing at 0.3%. It is likely that the economy grew by 0.2% in the fourth quarter. Even though the actual GDP components early next month, stronger net exports likely lifted the number of GDP. The Italian economy has performed relatively well compared to what investors predicted. December’s political referendum has shown to not harm businesses and consumers. At the same time, the banking sector (which was most feared to be impacted) has been operating at normal. If Donald Trump’s fiscal policy goes to what was promised, it would likely boost the Italian economy.

Euro Zone – Industrial Production (December)

Industrial Production in the Euro Zone likely contracted by 1.8% month-over-month and 1.3% year-over-year for December. This contraction essentially reverses most of the benefits that were seen in November’s gains. Germany could be the main factor for the contraction, since it showed that industrial output for the EU’s largest economy fell by 3% at the end of 2016. France and Spain also showed contractions, but of smaller amounts. Italy was the main contributor for strength in this data as the country showed production to be up 1.4% month-over-month.

Germany GDP (Q4)

Real GDP in Germany is believed to have expanded at the fastest pace seen in five years. It is likely that the German economy grew at 0.5% quarter-over-quarter and 1.8% year-over-year. This comes after a 0.2% quarter-over-quarter and 1.7% year-over-year growth in September. The sharp depreciation of the Euro in recent months has boosted exports towards the end of 2016. Similarly, consumer spending has been up and contributed to the expansion, though it is not sustainable as inflation is rising as well. The future of the economy is not so certain because of geopolitical risks domestically and internationally add to uncertainty.

Germany Consumer Price Index (January)

Consumer prices will show to rise 1.9% year-over-year at the start of this year, which is the highest rate of inflation growth in four years. Food and energy prices were the fastest to rise. Upward price pressure likely stems from higher commodity prices, instead of a surge in demand. German producers have to face the higher cost of imported goods since the Euro has depreciated. Similarly, higher prices for oils and metals have squeezed producer’s budgets.

While there is a chance that only some of the higher prices paid by producers have been passed on to consumers, over time, this would increase.

British Pound (GBP)

Consumer Price Index (January)

Headline inflation likely climbed to 2.2% year-over-year in January. Higher import prices that have been borne by producers need to be passed on to consumers. Following some clarity about the event of Brexit, the Pound gained some traction – however not enough. The Pound is still currently trading about 14% lower against the Dollar and 11% lower against the Euro since the referendum. Consumer price growth may continue to accelerate in the coming months and ultimately pass (if not already passed) the Bank of England’s 2% target. Data in the coming sessions will show.

Technical Analysis

Gold

As US stock markets gain traction and reach record highs, the Dollar benefits as well. This comes at the expense of gold, who has seen recent gains slowed down, and a drop in some value. Since this week, the price of gold has been falling. They reached a high of $1,244.71 and have been falling since (last week). It is not certain if the growth and recent uptick in the Dollar is sustainable, so which direction the price of gold will head. However, if there is more clarity in policies coming from America, then it is likely the price of gold will go down. The chart below shows how gold has been performing for the past year. The 10 day Exponential Moving Average has flattened.