Daily Insights Report 16/01/17

- 31 Mar 2017

16 Jan 2017

Trading markets in the US are closed today in observance of Martin Luther King Day.

Retail sales in the US increased 0.6% month over month in December, which is slightly below what the market expectations of 0.7% since there has been an increase in spending on gasoline and automobiles.

The University of Michigan consumer confidence index slipped in January. The index showed that the surge in confidence following the election result has clearly remained into the beginning of the New Year. With consumer confidence increasing and wage and employment growth staying solid – we can expect spending growth to increase in the coming months.

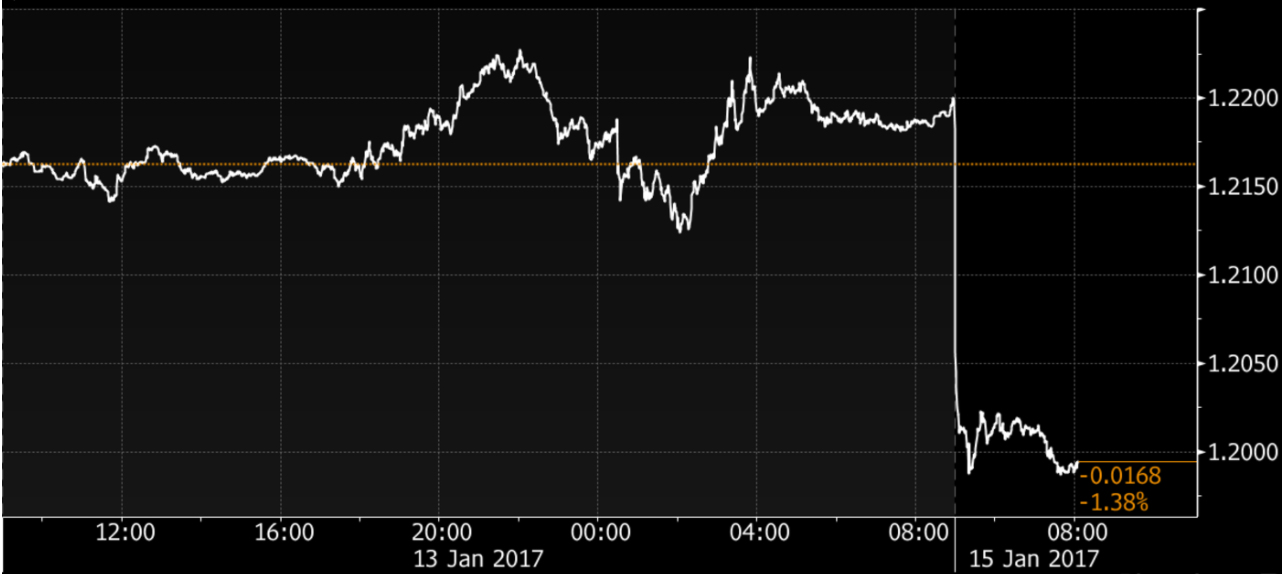

The value of the Pound fell after the Sunday Times newspaper reported that the Prime Minister will show plans to quit the European this week. The decline since Tuesday’s speech was about 1.6% (see graph below).

Since the decision to leave the EU, the value of the Pound has fallen by more than 19% against the Dollar. While there is no clear definition of a ‘hard’ or ‘soft’ Brexit, the market believes the first one is more likely. This idea means that the UK would give up full access to the single market and full access of the customs union along with the EU. This view supports those who voted for the UK to exit the EU. The Pound may rally if there are signals for a soft Brexit, which currently seems unlikely. Traders expect further depreciation of the Pound if there is more evidence of a Hard Brexit. Bank of America expects the Pound will drop to $1.15 in the first half of the year.

Faster US growth and higher interest rates are likely to increase the value of the USD. For emerging market currencies, the bigger issue would be protectionist policies

– The Pound dropped to as low as $1.1986, a level that has not been seen since October.

– The Yen rose 0.3% to 114.12 per Dollar.

– The Euro dropped 0.1% to $1.0632.

Commodities

– Oil rose 0.2% staying above the $52 per barrel level. After reaching a trade deal late in 2016, the next question important question is will the concerned parties reduce their supply by the amount they have stated. Supply data from last week show that the answer is still unsure. The price of oil is expected to fluctuate between the $50-$58 per barrel until this is fully resolved.

– Gold increased 0.5% and is currently at $1,207.77 an ounce. Since the election in the US, gold has risen almost consistently.

Euro (EUR)

Euro Zone External Trade

The Euro Zone’s trade surplus likely increased in November. Because of the depreciation of the Euro since the US election in October, exports must have benefitted outside of the single-currency area. This trend may continue further as policies suggested by the President-Elect would lead to an even higher Dollar – making the Euro zone more attractive as the US becomes less competitive.

Japanese Yen (JPY)

Industrial Activity indexes

Japan’s economic activity in industrials likely weakened for the month of November because of lower consumer spending. Some support for this comes as the Yen has gotten weaker, which would boost export-related services. Business related to wholesale and retail trade has suffered in domestic markets because consumers have decreased spending on big-ticket items. This is due to the weak growth in wage levels.

Technical Analysis

AUDJPY

Looking at the hourly chart of this currency pair, it seems there may be another uptrend in the current band. The value of 85.60 is at the value of the 100 day SMA (blue line). Looking at the stochastic indicators, it points to an oversold signal. Setting up a long trade with the parameters of the middle of the channel and a stop above the current 200 day SMA (red line)