Daily Insights Report 21/03/17

- 31 Mar 2017

21 Mar 2017

The Chicago Fed National Activity Index in the US rose to 0.34 in February from -0.02 in January. The improvement was seen in all the sub indexes of the index – including employment, sales, production, and housing.

The AUD hit a four month high overnight but lost this momentum and traction as a result of the RBA’s meeting minutes. The meeting minutes suggested the implications and risks of the booming housing market seen in the main urban cities of Australia.

The Dollar had a choppy session with the Dollar index falling to 100.02. This is the lowest level seen in over five weeks. The meeting of the G20 in Germany concluded with a statement that was notable with the commitment to avoid trade protectionism had been dropped. Historically, G20 meetings have a track record of increasing trade between member nations. It is believed that this is still the early days for the new presidential administration, so it is not sure to what extent protectionist policies will follow through. The next G20 meeting is scheduled to be in Germany in July. By then it is likely that uncertainties concerning the Trump administration are more clear.

– The GBP fell 0.3% against the Dollar to $1.2356 and fell 0.3% against the Euro to EUR 1.1500. This comes after the news that the UK prime minister (Theresa May) will trigger the two-year article 50 EU exit process next week.

Commodities

– With concerns about the high levels of the US crude inventories kept oil prices from gaining traction and increasing the price. Brent crude settled at $51.62 a barrel, representing a decline of 0.3%, but still higher than the three-month low of $50.25 it reached last week. West Texas Intermediate (WTI) crude was down by 1.2% to reach $48.21 a barrel.

– Gold was a benefactor of the Dollar’s weak performance. Gold has now seen its fourth consecutive day of gains. Currently, gold sits around $1,234 an ounce, which is a two-week high.

British Pound (GBP)

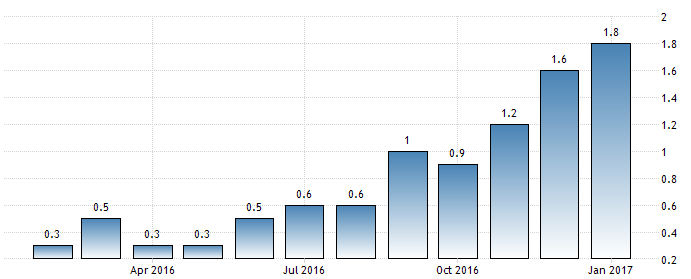

Consumer Price Index (February)

The UK’s annual headline inflation is believed to have accelerated to 2.2% year-over-year in February. This is since higher import prices made their way through to consumer prices. Even if the GBP recovered somewhat at the beginning of the year, it is still 15% lower against the Dollar and 11% lower against the Euro by the end of February since the time of the referendum decision. The most recent Markit PMI survey showed increases in average purchase prices in manufacturing at the beginning of 2017 increased. Input prices in the service sector rose at their highest pace since August 2008, and remained among the fastest in the history of the survey for manufacturing. Similarly, output prices showed the rate of increase to be near an 8-year high. Sellers seem to be passing the higher input prices onto their customers at a quicker rate than the policymakers have expected. A look at how the inflation rate has changed in the past year can be seen in the chart below.

Technical Analysis

USDCHF

Looking at the daily chart of this pair, we can see that the pair is having a difficult time passing through the 0.9950 area. This is in the middle of the rising channel that the pair has not broken since May of last year. Near the 200-day SMA, lies the 0.9900 area of interest. With an oversold stochastic signal, graphically it may suggest that the USD may appreciate against the CHF. As a result, aiming at previous highs may be an appropriate position to hold in this currency pair, especially near 1.03.