Daily Insights Report 23/02/23

- 31 Mar 2017

23 Feb 2017

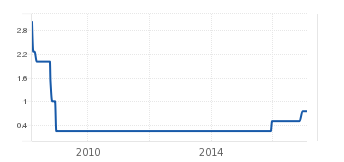

Officials from the Federal Reserve said it might be appropriate to raise the interest rates soon, but should wait to see data concerning the labor market and inflation. This was showed in yesterday’s release of FOMC Meeting Minutes. Policymakers mentioned because of the Dollar’s recent appreciation, it is uncertain which direction the Dollar will move as a result of the rate hike. Since it is an expectation, the impact of a federal rate hike may already be absorbed into the current price of the Dollar. A reminder of how the interest rate has changed in recent times is below.

Ultimately, the Dollar lost some value, because of the meeting minutes, but US treasury prices went higher. The Dollar index (basket of currencies measured against the USD) was down 0.2% at 101.18. Previously it was at 101.72.

There was very little change to the value of the Euro after German business confidence data came in very strong and inflation data showed to be at a four year high. German IFO business climate rose to 111.0 in February from 109.8 in the previous month.

Commodities

Generally, when the Dollar weakens, it helps commodity prices rise, since they are mostly denominated in USD.

– Brent crude oil settled at $55.84 a barrel, and fell 1.5% in yesterday’s day of trading. Similarly, West Texas Intermediate (WTI) crude was down 1.4% and reached $53.58.

– The softer Dollar helped gold increase $2 to $1,238 an ounce.

United States Dollar (USD)

New Home Sales (January)

There are an expected 575,000 new home sales in January. This comes after a ten month low seen in December. Even though the end of last year showed a decline, year-over-year the data still showed a 25% increase for the fourth quarter. There is a lot of room for further growth and this will likely be the trend this year. Transaction volumes are shown to be low. The most recent monthly data on new home sales is still 26% under the average for the last 20 years.

Technical Analysis

EURJPY

Looking at the daily chart of this currency pair, we can see that the pair is fluctuating between in a downward channel.

Recent positive economic data coming from the EU area has not been enough to drive up the value of the Euro. Similarly, there are events in the future which would typically weaken the currency, more than it already is. Most notably, concerns over the French election, and debt restructuring concerns coming from Greece and Italy.

As time continues on, the Euro may continue to weaken. A strategy would be to aim to allow the Yen to reach 107 per Euro before allowing the Euro to weaken further since the pair is near the upper boundary of the channel.