Daily Insights Report 10/01/17

- 29 Mar 2017

10 Jan 2017

Consumer credit in the US increased by $24.53 billion in November, following an upwardly revised $16.17 billion rise in October and beating market expectations of $18.48 billion. Revolving credit (credit that does not have a fixed number of payments) rose by $11.01 billion and non revolving credit went up by $13.52 billion.

Commodities

– West Texas Intermediate (WTI) crude was only slightly changed at $52 a barrel after falling 3.8% in the last session as an increase in US drilling offset signs that OPEC members are sticking to the planned output cuts. Monday’s decline was the biggest drop in more than 5 weeks after concern about Iraq’s commitment to the new deal.

– US oil inventories probably rose by 2 million barrels last week, according to a survey released before official government data being released on Wednesday.

– Gold was steady in the spot market at $1,181.48 an ounce with demand forecast to rise ahead of Chinese New Year. It gained 0.7% on Monday. Gold has increased in price for the fifth time in six days.

– Copper futures were little changed in New York ahead of Chinese prices data.

Euro (EUR)

France: Industrial Production (November)

France’s industrial production is likely to have increased 0.4% month-over-month in November, after decreasing 0.2% in the previous month. The PMI increased to a 67 month high in December, with output and new orders sharply increasing. Still, manufactured products in France lack higher sophistication. France’s trade balance is in surplus only for services related to tourism, slightly positive for agricultural products, and close to zero for intermediate goods.

The low quality of new fixed investment is partly to blame. Investment in automation as measured by the number of industrial robots, for example, has been lagging because French entrepreneurs are risk averse. In this regard, they are also fearful that they might not find a competent and skilled labor force, or unwisely rely on the already tarnished reputation of French products.

Australian Dollar (AUD)

Retail Sales

Australian households continue to spend in the final quarter of 2016, with retail sales likely expanding 0.4% over November. The low unemployment rate contradicts the weakness in the labor market, which is struggling to show wage growth and hurting household budgets. Low interest rates are providing some offset, but consumption growth will remain moderate at best in the coming months. The expectation for this data is 0.4%.

Japanese Yen (JPY)

Consumer Confidence – December

Better than expected data out of Japan in November suggests that consumer confidence likely increased in December to 41.4. However, the overall confidence level remains below the neutral mark, as wage growth remains very subtle. Inflation expectations are also set to rise on the back of the Yen depreciation and commodity prices.

Technical Analysis

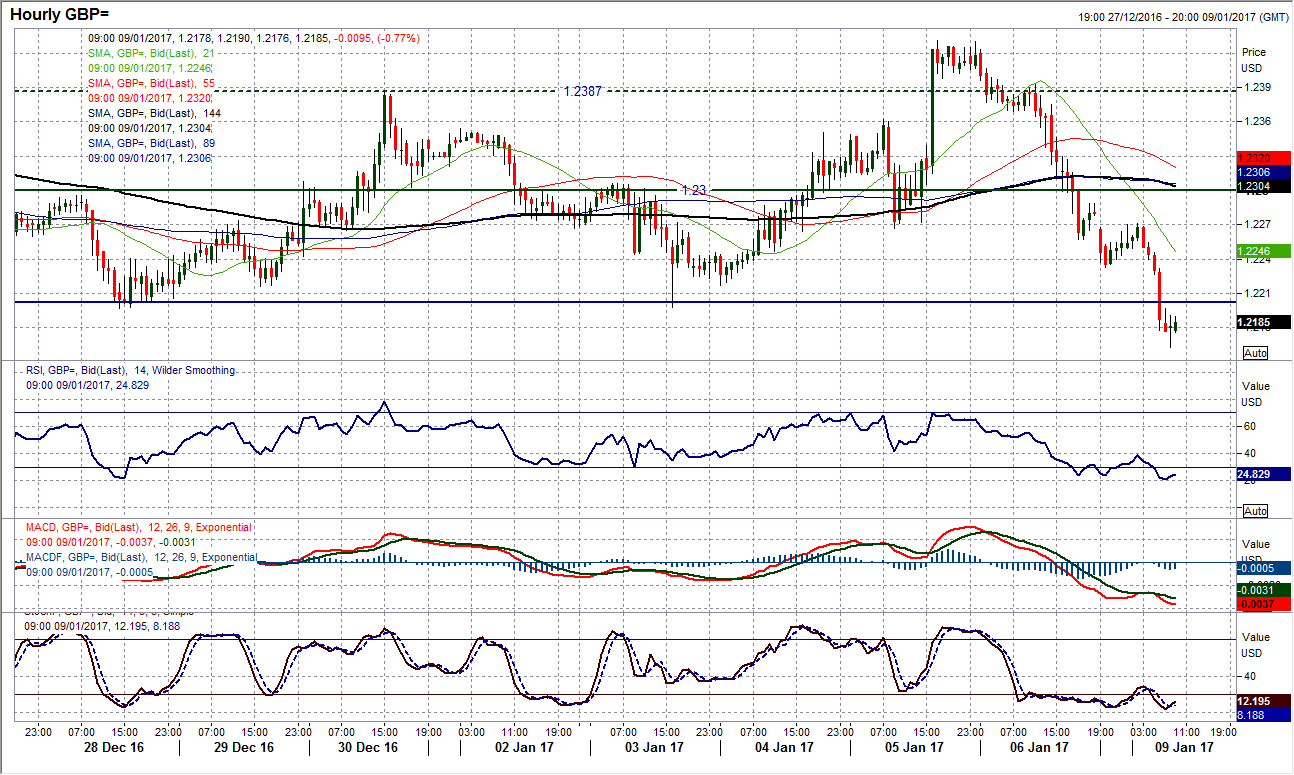

GBPUSD

The Pound continues to struggle on a relative basis. The recovery during the middle of last week has been blown away by the sharp selling pressure that came from Friday’s payroll report. The support level of $1.2197 that the market has been holding for the past couple of weeks has been broken and the market may be able to move towards $1.2080 which is the medium term range low.

Momentum indicators have turned negative once more with the RSI back under 40. A close below 1.2190 today could be seen as confirmation of the break.

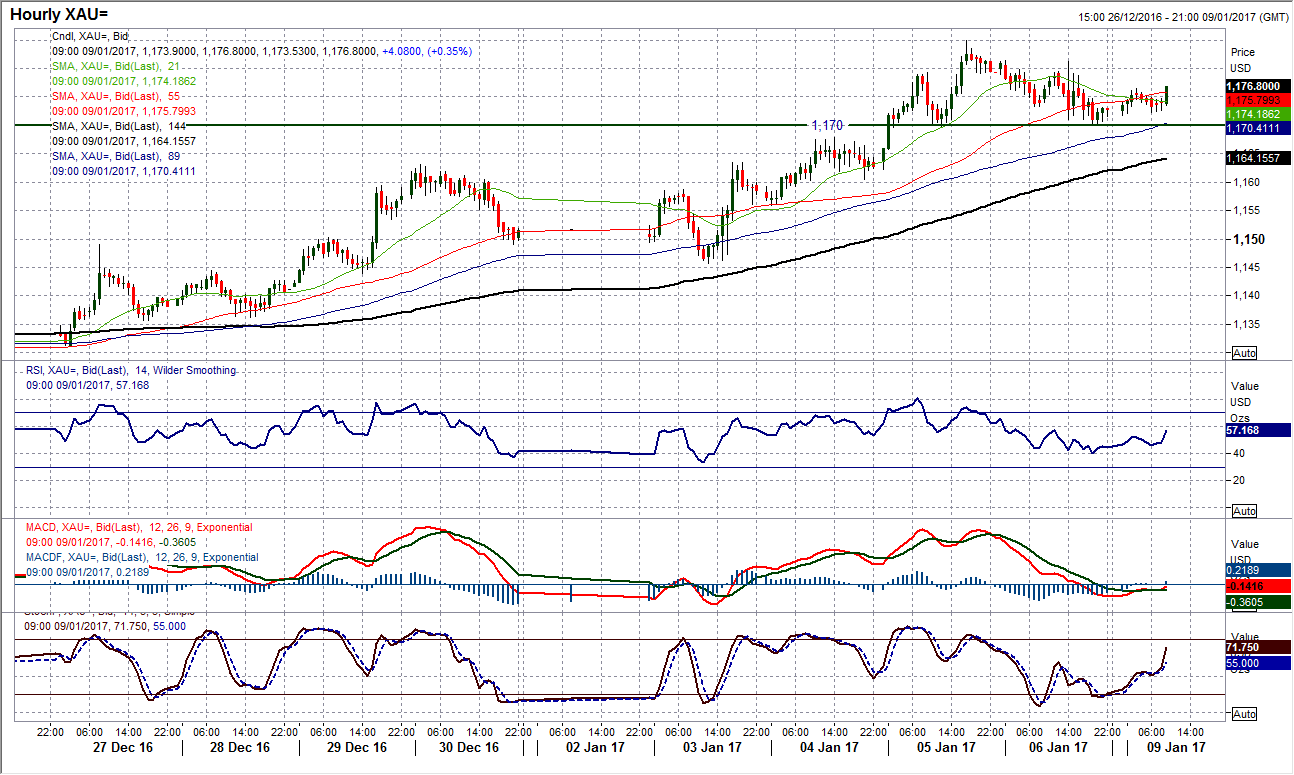

Gold

The recovery on the gold price seems to be important since the Non-farm Payrolls report on Friday. The resistance in the $1,180/$1,200 range is beginning to seem more important as the market reversed from $1,184.90 to currently trade around the old 61.8% Fibonacci retracement of $1,045/$1,375 rally. The hourly chart shows support at $1,170 which if reached would complete a small top pattern. The spoke high from the initial payrolls volatility is at $1,181 with $1,185 the new target.