Daily Insights Report 11/01/17

- 31 Mar 2017

11 Jan 2017

Wholesale stocks in the US jumped 1% month-over-month in November, recovering from a fall of 0.1% from the month before. Inventories of both durable and non-durable goods went up 1%. (Durable goods are those that do not quickly wear out, whereas nondurable goods wear out – usually in less than 3 years). Excluding automobiles, wholesale inventories increased 0.7%.

– The yen weakened 0.3% to 116.07 per Dollar after a two day increase of more than 1%. According to the famous Bloomberg Greenback Index, it shows that some of the gains of the Dollar in late 2016 have been erased. This index is comprised of 10 currencies, each of which has a different weight. The graph below shows this index.

– The Australian and New Zealand dollars were down at least 0.2%

Commodities

– West Texas Intermediate (WTI) crude gained 0.3% to $50.97 a barrel after sliding almost 6% over the past two days. Analysts predict US crude stockpiles rose by 1.5million barrels last week. This goes in the opposite direction of the optimism provided by countries stating they would cut production of crude oil. Supply data is scheduled to be released later today.

– Gold on the spot market fell 0.2% to $1,186.02 an ounce. This was the first time this week the value of gold went down.

– Copper went down 0.5% on the London Metal Exchange after increasing 3% on Tuesday.

It is believed that global growth this year will continue because of a rebound of commodity exporting countries and recovery in some advanced countries like the US. Fast US growth is likely to allow commodity exporting and developing countries to grow at an expected 2.3% this year. This comes after two years of stagnation for these countries.

Euro (EUR)

Spain Industrial Production

Spain’s industrial output likely added 0.9% year over year in November, and this was boosted by the now stable political situation at home and relatively strong manufacturing business activity in the Euro Zone. Spain’s manufacturing PMI strengthened to its best reading in November and once again in December. The number now stands solid at 55.3, due to higher output and new orders. The Euro Zone’s manufacturing PMI posted the strongest reading in December since April 2011. Improving business confidence after the resolution of the 10-month political deadlock with the formation of a minority government will support industrial output in the coming months. The slowdown in economic activity in Q3 was likely reversed because of more accommodating external conditions. We can expect industrial output to recover in the near term from the slowdown.

Technical Analysis.

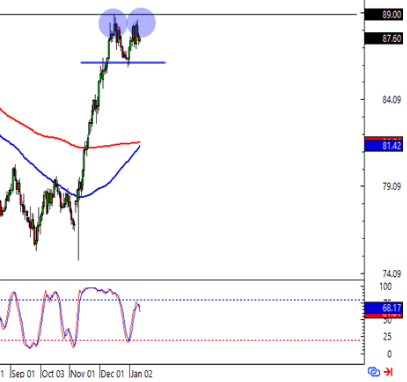

CADJPY

The Canadian Dollar has been shown to be the strongest currency in the G10, and the value of the currency has been shown to be strengthening. If looking at currency pairs, the CAD has remained strong against others including NZD and the GBP. The Canadian Dollar has been shown to be catching some gains from the USD since the President-Elect’s announcements about government spending.

There is uncertainty about the OPEC supply cuts and to what extent the oil price will change over the coming months. For this reason, the Canadian Dollar has potential to gain value. Historically, oil prices play an important role in determining the value of the CAD. Data released in Canada last Friday shows a positive outlook for the economy. Jobs report, and PMI figures were all shown to be better than expected. This could lead to a positive outcome from the Bank of Canada meeting next week, where an interest rate decision will be made. Looking at the Moving Average of different 100 and 200 days, we can see them almost crossing, which invites a trader to speculate. (blue shows the 100 day Simple Moving Average. red shows the 200 day Simple Moving Average).

Japanese data to be released this month is showing signs of optimism, but it may not be enough to offset speculation against this currency pair. A target range for this currency pair in the short run is in the 88.00 to 88.75 range.