Daily Insights Report 02/03/17

- 31 Mar 2017

2 Mar 2017

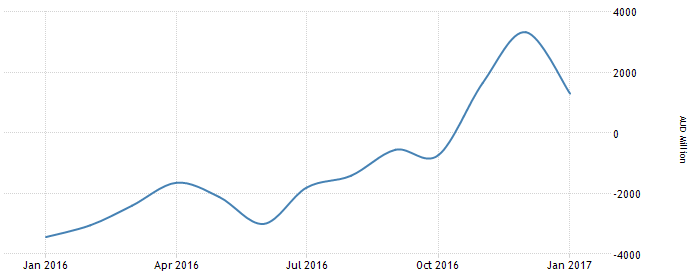

Australia’s Trade surplus fell to a 3-month low as shown by the most recent data release. The trade surplus narrowed by 61% to AUD 1.30 billion in January from 3.33 billion in December. Exports were shown to have fallen 3% while imports rose 4%. These two effects when combined can quickly reduce the surplus. The graph below shows how the trade surplus has weakened/strengthened over the last year.

With more evidence in the market of the Federal Reserve ready to interest rates this month, investors have freshly gained confidence in the strength of the US economy. This has pushed the stock market to record highs again. The graph below shows how the DJIA (Dow Jones Industrial Average) has improved in recent times. Since the time of the election, the index has continually risen.

The market now expects more than a 80% chance that the Fed will increase the interest rate. This comes after the head of the New York Federal Reserve (William Dudley) stated that increasing the interest rate is now “”a lot more compelling””.

Commodities

– Because the Dollar has strengthened slightly, Gold normally moves in the opposite direction. Gold prices fell but remained steady at $1,249 an ounce. Last Friday, gold reached the highest level in three months.

– Oil prices were up for a short amount of time but ended up coming down by 0.2% reaching $53.74 a barrel.

Euro (EUR)

Euro Zone – Unemployment (January)

Unemployment in the Euro Zone likely reached 9.5% in January from 9.6% in December. Year-over-year, the unemployment has improved in the Euro zone, as unemployment was 10.4% in January last year. Youth unemployment remains a growing problem in many European nations, and methods are being implemented to remedy the problem. While unemployment is expected to rise slightly because of political uncertainty and election worries, a stronger industrial output coming from Spain, Ireland, and Portugal is likely to help more.

CPI (February)

Harmonized inflation is likely to have increased to 1.9% in February from 1.8% in January. The recent increase is likely due to the increase in higher commodity prices. Combining economic growth with higher oil prices and a weaker Euro – will eventually lead to a higher inflation rate. It is unlikely that for the ECB to become hawkish before the end of the year – unless inflation effects grow out of control or commodity prices rise higher than expected.

Spain GDP (Q4)

Spain’s GDP is likely to have grown 3.0% year-over-year from the 4Q of 2016. While this is quite impressive, there is also a chance that this will be revised upwards because of significant improvements seen in the past two months, and now being estimated as a strengthening economy in the Euro Zone. Because of more clarity in the political sphere, producer and consumer sentiment has started to improve. Labor market recovery and high PMI results show that economic activity has grown and is likely to continue growing in the middle-long term.

Technical Analysis

USD/CAD

Looking at the 4-hour chart of this currency pair we can note that the USD has had sharp periods of appreciation against the CAD. Notable events include the election, and now the potential interest rise. Through the appreciation episodes, the value of the pair has remained almost always within the channel. It is likely that the pair is about to reach the 1.3375 level – which is at the middle of the channel. Similarly, the stochastic indicators are showing that it is deep into the overbought area. A shorting strategy could be used around the 1.3000 level.