Daily Insights Report 03/03/17

- 31 Mar 2017

3 Mar 2017

The Caixin China Services PMI fell to 52.6 in February from 53.1 in January. While this is the lowest growth seen since October 2016, it has not been enough to rattle financial markets elsewhere. Output and new orders rose slowly, whereas employment increased and business sentiment reached a 21-month high. The graph below shows the past year’s performance of this index.

US stocks fell slightly after reaching record highs this week. The 1.4% gain that led to the record high came after a speech by the President. This was the biggest one day gain since before the election was concluded. The overall speech was optimistic about the growth potential of the US.

Data released earlier today from Japan showed that the country has returned to inflation for the first time since 2015. This comes after the price of energy rose 9.2%, after falling strongly in the year of 2016. Japan has been able to steer away from deflation episodes since Mr. Abe assuming his role in 2012. While it is unsure if the economy will be able to reach the Bank of Japan target inflation of 2.0%, it is likely that the economy will grow.

Commodities

– Gold dropped by the most in three months. It lost 1.4% and settled at $1,232.90 an ounce (a price drop of about $13). February 24th marks a point for traders as a method of resistance. It was the highest price of gold seen for more than three months.

– Oil prices fell for a third consecutive day. This is the worst performance of the commodity in two months. Oil prices have become jeopardized because of record high stockpiles in the US. Similarly, with time, the plan to materialize shale oil production will hurt the price of crude oil in the global marketplace. West Texas Intermediate (WTI) crude fell 2.2% and reached $52.67 a barrel.

– The CAD weakened 0.5% as the price of oil fell. This shows the power of the price of oil in Canada, because data showed that Canada to have faster than expected economic growth.

– The Euro fell for a third consecutive day to the amount of 0.4% to reach $1.0506.

United States Dollar (USD)

ISM Non-Manufacturing Index (February)

This data is a survey of about 400 purchasing managers who are asked to rate the relative level of business conditions. These include but are not limited to production, employment, prices, supplier deliveries, and inventories.

The expectation for this data is 56.5. The index should show some traction from the time of the Presidential Election because demand for domestic services remains high. A cause for concern for the production managers is that cost pressures are rising quickly and this can impact production decisions. In January, the Non-Manufacturing index on prices showed that prices had reached a 30-month high in January.

Technical Analysis

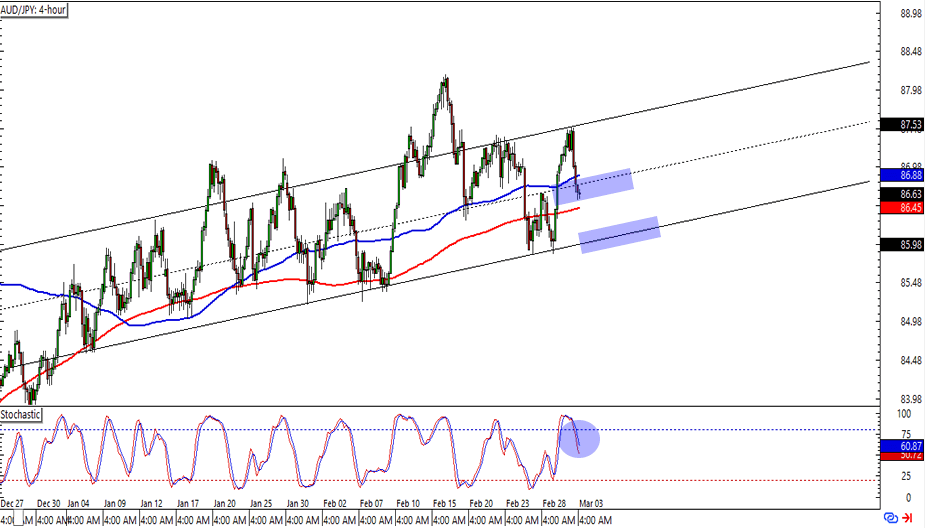

AUDJPY

Looking at the 4-hour chart of this pair, we can see the pair moving in a somewhat narrow channel. While the Yen has recently appreciated, it is not certain for how long this might be sustained. While it may be seen as a new era in the Japanese economy because of the recent inflation data, the fact has not changed that the currency recently been volatile and vulnerable to varied data releases.

The JPY may go through some hiccups and fluctuations in the short term because of a confirmation of this new direction of the economy. For this reason, a strategy which allows the JPY to depreciate to a level around 87.00 could be viable.