Daily Insights Report 07/03/17

- 31 Mar 2017

7 Mar 2017

New orders for manufactured goods in the US increased 1.2% after December’s 1.3%. This is significantly higher than the market expectation of 0.2%. Orders for transportation equipment increased by 6.2%. At the same time, there was a large increase (over 60%) for civilian and defense aircrafts.

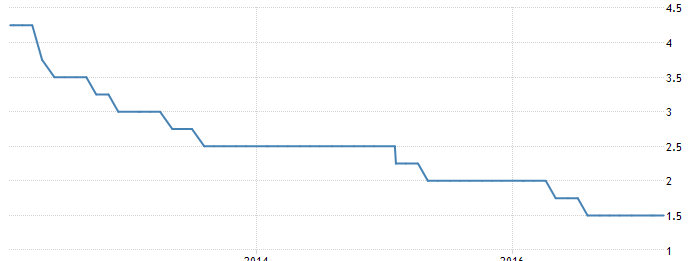

The Reserve Bank of Australia left the cash rate steady at a record low of 1.5% during the most recent meeting. This was expected by the market. Inflation is expected to surpass the 2.0% threshold this year, and policymakers stated that not changing the interest rate would be appropriate given the level of growth in the economy. A look at how interest rates in Australia have changed over the last five years can be seen below.

Commodities

– Gold fell 0.8% and reached $1,225.45 after the USD appreciated slightly.

– Oil prices fell in recent trading. Brent crude lost 0.1% and fell to $55.91 a barrel. At the same time, West Texas Intermediate (WTI) fell 0.3% to reach $53.18 a barrel.

– The US Dollar is mixed after last week’s interest rate updates. The Dollar is now within 2% of a 14-year high. Estimates are as high as 86.4% that the Federal Reserve will increase the interest rate by 25 basis points on March 15.

– The Dollar appreciated against the Euro by 0.4%. The Single currency took a small hit after news surfaced that Alain Juppe will not be replacing Francois Fillon as the centre-right candidate in the French presidential election. The election is expected to start with a first round vote at the end of April.

United States Dollar (USD)

Trade Balance (January)

The expectation for this data is currently -$45.7 billion in a trade deficit. It is likely that the trade worsened in January since the report on recent goods showed that there had been a decline in imports. Even though the trade gap is growing, exports are again adding to US output instead of being a drag on growth. Exports rose to a two-year high of 1.8% year-over-year in Q4 of last year. Similarly, December’s 2.7% monthly advance was the highest result seen in four years.

Euro (EUR)

GDP (Q4)

Preliminary data showed that the real GDP in the Euro Zone expanded by 0.4% quarter over quarter in Q4. The yearly amount of growth was 1.7%. Because the preliminary report did not show the expenditure statistics, it is likely that domestic demand, especially investment and consumer spending are what powered growth. The overall effect is still negative, because of the weaker Euro.

Even though the economy should expand at the same pace of what it did in 2016, there are some events looming in the near future that could hurt the Euro. Most notably political anxiety about the 2017 voting season, tough negotiations over the UK’s exit from the EU which could ultimately hurt trade. Some traction could be found from the American economy which has continued to strengthen in recent months. Similarly, a new fiscal policy would help the Euro Zone as a whole.

Technical Analysis

GBPUSD

This pair has fallen heavily in the latter part of the previous year. Recent trading values have shown that it has fluctuated between the 1.22 and 1.27 area. Looking at the daily chart, we are able to see a bearish pennant, which in theory suggests that the a direction change may occur. However the moving averages of different periods are pointing to the direction remaining consistent and going lower in the future. With the recent appreciation from the USD because of interest rate discussion, it is likely that the USD may retain its value. Data scheduled to be released by the end of the week will likely confirm this statement.