Daily Insights Report 09/03/17

- 31 Mar 2017

9 Mar 2017

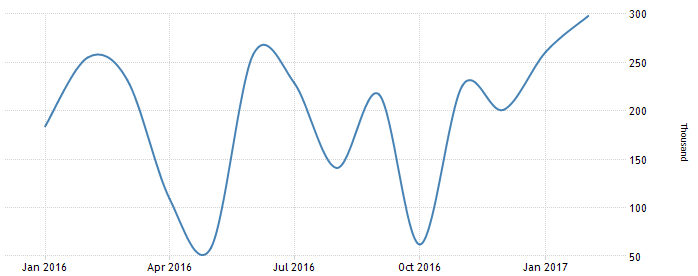

Private businesses in the US showed to hire 298,000 workers in February compared to the already upwardly revised 261,000 in January. This was already well above the market expectations of 190,000. The service industry added 193,000 new jobs and the production sector added 106,000. The graph below can show that the job market has almost consistently been improving since October.

Commodities

– Gold was steady after a slump in prices that lasted three days. It remained to fluctuate to small degrees around the $1,208.01 an ounce level.

– Oil prices fell on Wednesday by their most amount in a single year after data from US crude inventories showed that their inventory climbed for the ninth straight week to a new high. West Texas Intermediate (WTI) crude fell by about 5.8% to reach $50.28 a barrel. Brent on the other hand fell 4.9% to reach $53.10 a barrel. This is the lowest level seen since November. The report came the day after Khalid al-Falih (oil minister of Saudi Arabia) stated that OPEC’s efforts to stabilize crude prices may be in jeopardy because the new oil price actually has given more incentive for US shale producers to join production.

As a result of this, currencies of oil exporting countries took a hit. These include the Russian Rouble, South African Rand, Canadian Dollar and Norwegian Krone. In fact, the Canadian Dollar was down 0.6% against the Dollar, settling at 1.35, the lowest value of the year so far.

Euro (EUR)

Monetary Policy (March)

Even though there is rising inflation at the moment in the Euro zone, raising the interest rate may not be an efficient choice. This is because an increase in the interest rate may in fact un do any of the positive trends that has already been seen in Euro Zone. With a forecast of a lot of political risks in the different countries, raising the interest rate may induce a higher savings rate. With quantitative easing scheduled to be over this year, it may be that the ECB raises interest rates later.

Australian Dollar (AUD)

Housing Finance (January)

The expectation for this data is -1.8%. The number of owner-occupied housing finance commitments is likely to have fallen in January, though the overall demand remains strong. The housing market in the two main centers including Sydney and Melbourne continue to grow quickly, leading some to believe of a housing bubble being formed. Other places, including Brisbane and Perth struggle to gain traction in their housing markets. Perth’s real estate market is especially going through a difficult time because of the mining downtown in the region. Since lending requirements have been tightened in recent times, and investors face higher interest rates, the housing market will need some time before gaining solid traction in Australia.

Technical Analysis

GBPNZD

Looking at the daily chart of the GBP/NZD, we can see a bearish wedge pattern. Given the economic situation of the British economy, it is currently weak, and the market predicts that it may weaken further in the near future. For this reason, shorting this currency may be an effective strategy with this pair.