Daily Insights Report 15/03/17

- 31 Mar 2017

15 Mar 2017

US producer prices showed to have grown 0.3% month-over-month in February, after rising 0.6% in January. This growth is more than what was expected, and small signs like this are what trigger inflation in the future as producers pass on the higher prices to consumers. Excluding food, energy, and trade services – prices increased by 0.3%, which is the largest growth since April 2016.

– The GBP was the biggest loser in yesterday’s trading, as it weakened by almost 0.9% in a single day before reducing the losses to 0.5%.

– The Euro fell 0.2% to reach $1.0637 after falling by an equal 0.2% on Monday as well.

Commodities

– For the first time of the year, Brent crude came before the $50 mark. This comes after OPEC raised their estimates for oil production outside of the cartel. West Texas Intermediate (WTI) crude was down 1% to reach $47.94. Because of this, Saudi Arabia’s energy minister gave a rare statement on Tuesday stating the commitment of the country to stabilizing the global oil market. How this plays out in the coming week will be interesting, as US shale production continues to grow.

– Gold decreased slightly as the Dollar appreciated. The metal was down $5 and reached $1,198 per ounce. This is the lowest close it has seen since the end of January.

– Copper, which is often seen as a gauge for the world economy, rose 0.4% to $5,820 a ton.

British Pound (GBP)

Unemployment (February)

Headline unemployment is likely to be unchanged at 4.8% in the three months leading to January. Which is the lowest since the mid-2005 level. December’s labor market data showed to be performing better than expected. Although the number of job vacancies increased slightly in January’s data, the claimant count decreased by 42,400 claims. December saw claimants decrease by 20,500. Job surveys showed a growth in both permanent and temporary job placements.

PMI data showed to a continued rise in jobs in the services, manufacturing, and construction sectors. There are signals of a growing future with less unemployment. Labor markets tend to change with a lag with respect to the overall economy. With uncertainty looming because of the upcoming event of Brexit, it is not certain which direction the labor market will move in the medium term.

Euro (EUR)

Italy – Consumer Price Index (February)

Estimates show that inflation in Italy are at 1.6% in February, after increasing 1% in the previous month. The fast change likely comes from higher transport prices and higher unprocessed food prices. Core inflation, which excludes energy and seasonal food products increased to 0.7% year-over year from 0.5% in January. Even though the consumer price index showed some acceleration, the core inflation remained relatively stable. With unemployment slightly edging upwards, it is leading to some demand-driven inflation, which is likely the case for the 0.2% differential.

Even though the economy has been growing since 2014, the jobless rate has been rising since the beginning of 2016. This is likely what is holding wages from increasing.

France – Consumer Price Index (February)

France’s CPI inflation likely decelerated in February even though energy prices have not been stable, but domestic demand has been in recovery. It is likely that the 0.2% month-over-month rise will be seen. Even though oil prices are currently at lows, in year-over-year terms they have appreciated strongly. This is what would likely what kept inflation from falling in France.

France’s manufacturing PMI rose to a 66-month high, with new businesses and jobs. We can expect prices to gain further momentum in the coming months.

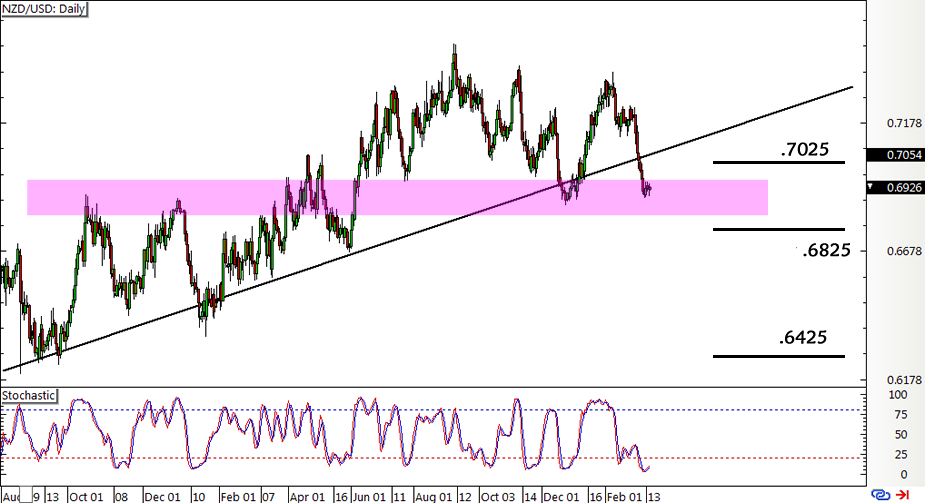

Technical Analysis

NZDUSD

Looking at the daily chart of the NZDUSD on the day that the FOMC may raise interest rates may provide a trading opportunity. Even though it is likely the Fed’s decision to increase the interest rate is already priced into the USD, it may give it a slight upward push once it is finally happens. This is because of the upgraded growth and inflation forecasts and the fact that the Fed would be on chart for completing the three rate hikes this year. The NZD will be releasing the Q4GDP few hours after the FOMC meeting. This may cause some downward pressure on the NZD because weaker growth is expected to be seen.

A strategy that may be profitable for this pair is to short the pair at 0.6825