Daily Insights Report 14/03/17

- 31 Mar 2017

14 Mar 2017

Industrial production in Italy fell by 2.3% in January. This is the biggest drop since January of 2012. In December, this data actually rose by 1.4%. Output of consumer, intermediate, and capital goods fell, but production for energy actually rose.

The NAB (National Australia Bank) confidence index in Australia dropped to 7 in February of 2017 from 10 in the previous month. Other metrics from this index also showed to have weakened, most notably trading which fell from 23 to 13.

Last Friday’s employment report is likely what will give the Fed a green light for increasing the interest rate this week. Because of this, the current price of the Dollar may have already absorbed the interest rate hike. When a country increases the interest rate, it typically sees the currency appreciate because the demand goes up for the currency. Demand for the currency goes up because now investors can receive more by holding the currency.

– The GBP gained 0.5% and was at $1.2228. Prime Minister Theresa May wants to go ahead and begin the proceedings concerning Brexit.

– The EUR was down 0.1% at $1.0655 as the markets awaited the outcome of the Dutch vote. While it was unlikely that this be a significant event to impact financial markets so drastically, though it is the introduction to other elections coming up in Europe in the near future.

Commodities

– Oil prices were more stable on Monday even though the price of oil fell significantly last week. West Texas Intermediate (WTI) crude came and settled around the $48.45 per barrel level. Brent crude on the other hand passed the $50 mark and was reached $51.35.

– Gold, while sitting near a five-week low level, remained relatively stable at $1,204 an ounce.

Euro (EUR)

Germany – Consumer Price Index (February)

Early estimates show that Germany’s consumer prices rose 2.2% year-over-year in February. This has been the fastest pace since August 2012, which has surpassed the ECB’s target of 2.0%. Energy prices climbed 7.2% year-over-year, with a boost coming from the 5.9% increase from January. Though recent developments in the oil market make it unsure which direction will the price of oil move, arguably the most important constituent of energy inputs.

The weaker Euro has also contributed to the price of imported goods to increase. Higher prices for metals, made it more expensive for German producers, and this can be seen in the almost six year high cost reported in the Markit manufacturing PMI data. Lastly, a harsh winter that was seen in south Europe, likely increased the prices for some agricultural products.

Germany ZEW Indicator of Economic Sentiment (March)

Business sentiment in Germany, dropped in February to 10.4, even though it had improved in the month of January. For March, it is likely that the data will show an increase, with the data reaching 12. The strong labor market shows a potential upward tick in business confidence. Seasonally adjusted unemployment showed to keep steady at the 5.9% in February.

Markit manufacturing PMI jumped to a 69-month high, showing better business conditions. However, increasing geopolitical tensions and inflation, combined with the slowdown of GDP growth may negatively impact business sentiment in the long run. This month’s data may be a highpoint for the near future.

Technical Analysis

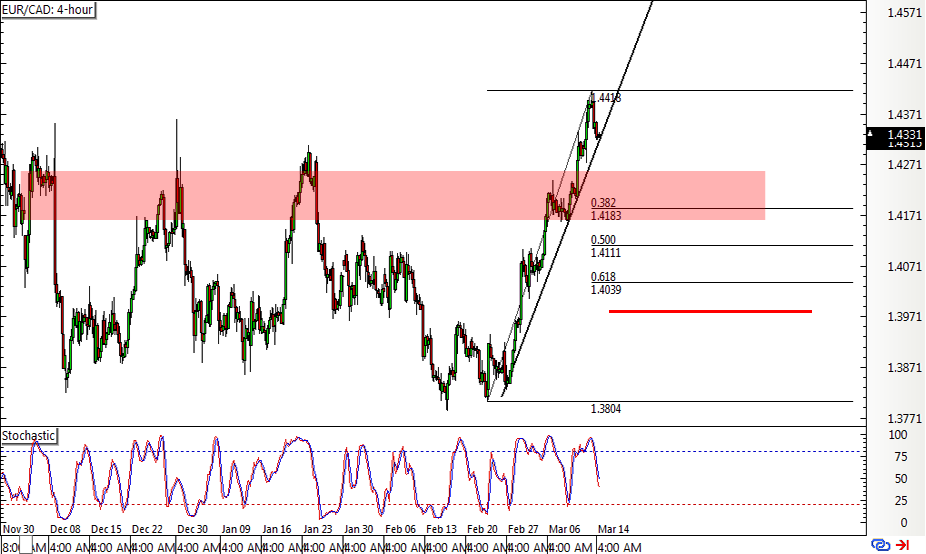

EURCAD

A few days ago, the EURCAD broke out of the long-term resistance around the 1.42 – 1.4250 area, likely due to developments in the US oil market. Using the Fibonacci retracement tool on the 4-hour chart, the 38.2% retracement is close to 1.42. Looking at the stochastic indicators, it can be suggested that there might a change of direction. A potential trading position worth entering might be to keep a long position against the EUR/CAD pair with a target of 1.4330.