Daily Insights Report 28/03/17

- 31 Mar 2017

28 Mar 2017

US stock markets closed with mixed sentiment after Monday’s day of trading. This comes after there was a sharp drop at the time the market opened. The unclear sentiment comes from President Trump’s failure to repeal Obamacare last week. As a result, the Dow Jones closed 46 points lower to reach 20,551 (a drop of 0.2%). This is the 8th consecutive fall,

– The Japanese Yen was 0.1% stronger against the Dollar at 110.6, on target to strengthen for ten out of the last eleven trading sessions. This is since investors have shifted to other assets since the USD has lost some traction.

– The AUD was up 0.2% against the USD at $0.7632.

– The GBP was up 0.1% at $1.2568 while the Euro remained flat at $1.0865. This happened before tomorrow when the UK will invoke Article 50 to give formal notice of its intention to leave the EU.

Commodities

– Gold was marginally lower at $1,253.94 an ounce after gaining 0.9% on Monday in its biggest one-day gain in two-weeks.

– Oil prices showed to strengthen slightly. Brent crude was up 0.3% to reach $50.92 a barrel. At the same time, West Texas Intermediate (WTI) crude rose 0.4% to reach $47.94 per barrel.

United States Dollar (USD)

S&P Case-Shiller Home Price Index (January)

The expectation for this data is a 5.7% yearly change of the 20-city index. Gains in home sales over the long-term whilst having a tight supply can keep the this index rising ahead of 5.0% per-year in January. Nationally home prices lag the pre-crisis levels by about 7%, since certain local markets are considered overvalued. However, consistent price gains have reduced the amount of homeowners that have gone underwater on their mortgages, which has kept the housing market slightly more stable at the same time. Tighter reforms and more lending requirements may continue to keep the housing market growing at a healthy rate.

Euro (EUR)

Germany – Retail Sales (February)

Germany’s retail sector likely recovered somewhat in February after seeing a sharp contraction at the beginning of the year. Sales are expected to have increased by 0.2% month-over-month from January, when they had fallen 0.8%. However, compared to the previous year, sales have fallen. The Markit retail PMI rose to 51.2 in January from 50.3 in December, suggesting that there will be a slightly stronger growth in retail sales. Consumption expenditure powered the country’s expansion last year, while other components of GDP have not performed as well. Conservative German households will not likely increase their spending by much in coming months because the outlook remains uncertain due to the accelerating inflation. Germany’s annual national measure of inflation accelerated to 2.1% in February, which is the fastest pace of increase since May 2012.

Germany Unemployment (March)

Germany’s seasonally adjusted unemployment rate likely remained at 5.9% in March for a third consecutive month, after it fell to this record low level in January. German’s businesses have shown signs that they will remain confident in the country’s expansion, since they have increased their labor force, even though there are uncertainties and many geopolitical tensions in the region. Details of the latest Markit manufacturing PMI showed that the rate of hiring accelerated to one of the fastest seen in more than five years. The weakening Euro, which has boosted exports at the end of last year, should also help increase the demand for German products, which would ideally lead to higher employment figures. A slight bump up in unemployment is expected because of the flow of refugees into the country who are deemed to be part of the German labor force.

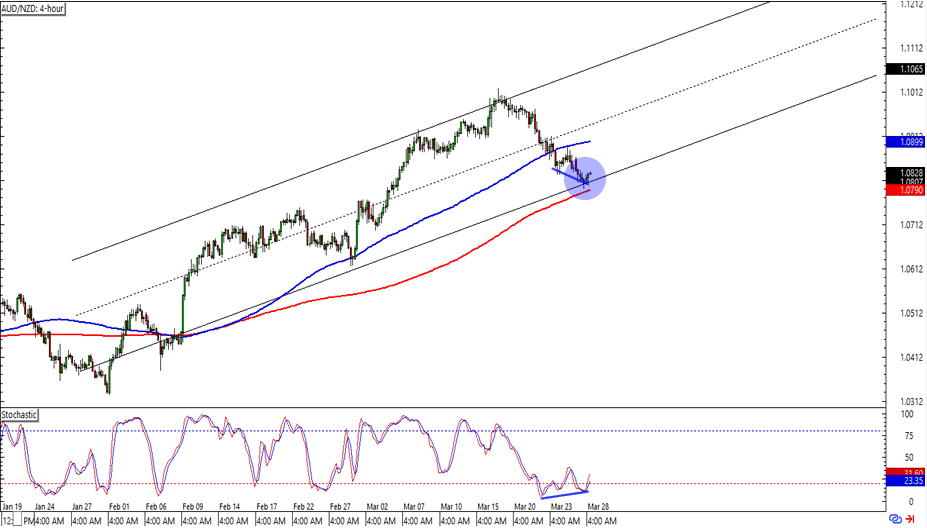

Technical Analysis

AUDNZD

Looking at the 4-hour chart of this currency pair, it shows a bullish divergence that suggests that a trading opportunity exists. The pair is currently around the 1.0800 level which is in the middle of a rising channel and the 200 SMA support area. With this in mind, a long position may have more potential with this pair. The AUD may strengthen against the NZD, due to positive data scheduled to release later in the week, so it may be viable to enter a trading position now.