Daily Insights Report 29/03/17

- 31 Mar 2017

29 Mar 2017

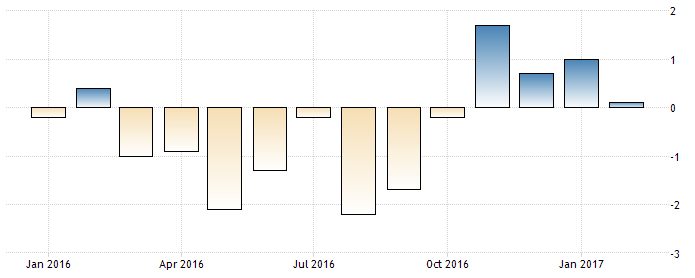

Retail sales in Japan showed to have risen by 0.1% year-over-year- in February 2017, after a 1.0% increase in the previous month. This is still the weakest rise seen since October 2016. This can also be seen in the chart below. Continually seeing data of this nature in the near future would suggest that Japan is still having a tough time economically, and as a result, the long term value of the JPY may decline.

– There was a slight improvement in the Dollar after it recently fell to multi-month lows against the Euro and the Yen. Part of this is related to the release of some encouraging economic data released in the country. The Dollar index (where the Dollar is measured against a basket of ten currencies) was up 0.6% as the Euro weakened 0.5% against the Dollar to reach $1.0810. The USD also gained 0.4% against the JPY to reach 111.14. The vice-chair of the Fed (Stanley Fischer) stated on Tuesday that there would be two more rate rises in 2017. The Fed’s recent increase of 25 basis points happened two weeks ago and the Fed has kept a forecast for increasing the interest rate two times for 25 basis points each time by the end of the year.

– Weakness from the GBP likely stems from the beginning of Article 50, which is the formal method for the UK to quit the EU. Early losses for the Pound were seen after the Scottish parliament supported a second independence referendum that would separate Scotland from the rest of the UK. The Pound has been seen to be losing against the Dollar this morning and fell 0.3% this morning alone to reach $1.241. Until now, it has lost 1.2% over the last two-days. As of this morning, it is the only currency that has weakened against the Dollar. Currencies including the JPY and AUD have strengthened.

Commodities

– Energy stocks were trading for higher values across different equity markets as oil prices reached their highest level seen for a week. Brent crude settled at $51.33 a barrel, which represents a 1.1% gain. At the same time, West Texas Intermediate (WTI) crude was up 1.2% and reached $48.33.

– Gold, rose to the price of $1,258 an ounce, but the gain was short-lived. Strength given from the USD kept gold from rising and then led to gold reaching down to $1,250 by the end of the trading day.

United States Dollar (USD)

Pending Home Sales Index (February)

The expectation for this data is to rise to 2.4%. This is after this data fell to a 12-month low in January. Though sales and home lending are on a long-term uptrend, the pace of gains has not been consistent. Uneven results imply that when interest and mortgage rates rise, it can negatively impact the housing market since less people will be interested as the cost of borrowing funds is higher.

Technical Analysis

CADJPY

In recent days, the Japanese Yen has shown to be outperforming other major currencies. Since the drop in US bond yields, and downward pressure on the Dollar because of the Trump administration, The JPY has been behaving as a safe-haven currency before the Article 50 is underway. Looking at the 4-hour chart of this current pair, it can be seen a descending channel could keep its ground and the price is continuing to follow this trend.

A potential drawback to betting against the CAD is because of the developments in the oil and energy market recently. Oil-related headlines have been showing an increase in stockpiles, more rig counts, and general issues stemming from OPEC members regarding their output. As a result of these three, it gives leeway for the CAD to appreciate in the long term.