Daily Insights Report 28/04/17

- 28 Apr 2017

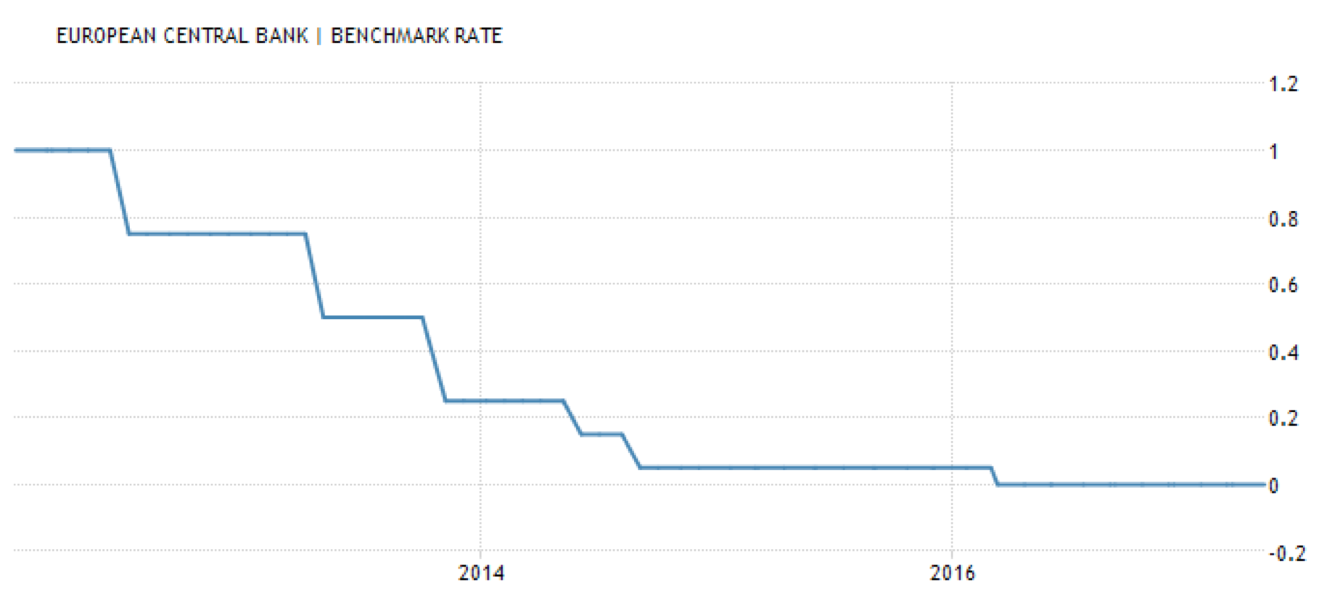

The ECB left the monetary policy unchanged. They held their benchmark refinancing rate at 0% and the pace of its bond-purchases at EUR 60B on April 27th. President Draghi said that the Eurozone recovery is becoming more solid and downside risks have diminished although he is not totally confident in inflation converging to the target level. In the past 5 years, the benchmark rate has been shown to be decreasing until reaching the 0% level.

The president of the ECB gave a more upbeat assessment of the Eurozone’s economic performance but repeated that inflation outlook remained unchanged. There was very little new information that was released in his comments. Through the start of the week, the Euro had rallied strongly as the outcome of the first round of the French presidential election helped soothe recent concerns about European political risk.

-The USD was seen to be rather stable against the CAD at C$1.3617. This comes after uncertainty increased about the future of NAFTA in its current form.

– US Treasuries have had a quiet session with the yield of 10-year T bills down 2 basis points to reach 2.29%. Because of this, the USD appreciated against the Yen by 0.1% to reach 111.17.

Commodities

– Energy stocks performed poorly on both sides of the Atlantic Ocean. This comes after the price of gasoline fell. Brent crude settled at $51.44 a barrel, which is down 0.7%. West Texas Intermediate (WTI) crude was 0.8% lower in late trading to reach $49.21.

– Because of a slightly stronger Dollar – gold weakened. It was pushed down by $4 to reach $1,264 an ounce.

Euro (EUR)

France GDP (Q1)

The French economy likely grew 0.3% quarter-over-quarter in the three months to March, decelerating slightly from 0.4% in the previous quarter. Household consumption likely drove the expansion, while net exports dragged on the final reading. The annual expansion rate accelerated to 1.3% from 1.1% in the three months to December, but this is lower than what was expected. French consumer and business confidence is slowly improving. This reflects a strengthening labor market and a slowly firming recovery in the general economy, as well as fewer fears about the consequences of Brexit. Still, with lack of productive investment and an ageing population, France currently lacks a sustainable growth engine. Also, the looming presidential elections posed both a threat in this quarter. While it is not fully resolved yet, there is much more clarity in the situation with the likelihood of Macron winning.

German Retail Sales (March)

German retail sales likely dipped in March following an unexpected increase in the previous month. Sales likely have decreased by 0.5% m/m from February, when they increased by 1.8%. The Markit retail PMI climbed further to 52.5 in March from 51.2 in the previous month, suggesting stronger growth of retail sales in coming months. Consumption expenditure powered the country’s expansion last year, however the other parts of GDP remained stagnant. Conservative German households will likely not ramp up their spending in coming months, because the outlook remains uncertain and tangled with the accelerating inflation. Although Germany’s annual national measure of inflation decelerated to 1.7% in March from 2.1% in February, rising commodity prices and a weak euro should support price growth in the coming months.

France Household Consumption (March)

French household expenditures on goods likely increased up 0.2% month-over-month in March, after subtracting 0.8% February. Still-low oil prices as well as low prices of most goods, an improving labor market, slow recovery in the country are lifting consumption on a yearly basis. The retail PMI, however, fell into contractionary territory, falling to 49.4 in March from 51.7 in the February. Although employment increased, gross margins were still squeezed by a pickup in the rate of wholesale price inflation. The PMI drop could be attributed to uncertainty before the upcoming presidential elections, as most retailers failed to meet their sales target. With the election uncertainty almost subsided, it gives way for a more productive future. Still, French households are careful and their savings remain high (close to 15%), limiting discretionary spending.

Technical Analysis

EURUSD

Looking at the four-hour chart of this currency pair, there is a chance to enter a trading position against the countertrend. Technical indicators are showing that the Euro could retreat from its climb. Stochastic indicators can accommodate the pair further before reaching the oversold values. The 100 day SMA is still below the 200 day SMA in this time-horizon. Shorting the currency pair at this time would be a viable strategy.