Daily Insights Report 15/02/17

- 31 Mar 2017

15 Feb 2017

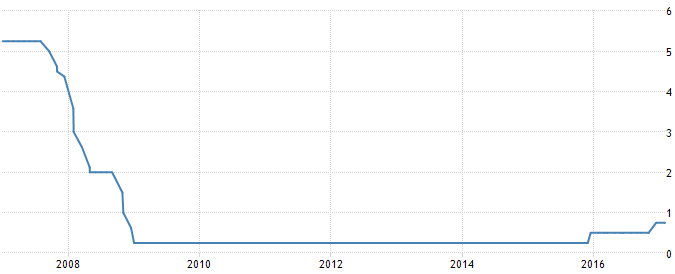

The US economy is expected to continue growing at a stable pace, and waiting too long would not be the right decision, said Janet Yellen to the Congress. She mentioned that both the economic outlook and fiscal policy face uncertainty and changes in monetary policy will depend on incoming data that will be released. A reminder of how US interest rates have changed in recent years can be seen in the graph below. Estimates state that the chance for an increase in the interest rate next month climbed as a result of Janet Yellen’s comments, and are now 34%.

Commodities

– Brent Crude Oil fell 0.34% and was trading at 55.63 a barrel. Meanwhile, West Texas Intermediate (WTI) crude trades at $52.84 a barrel.

– Gold changed slightly and increased by 0.13% to reach $1,227.10 per ounce.

United States Dollar (USD)

Consumer Price Index (January)

Higher gasoline prices can give a slight bump to the CPI, and allow it to grow for the sixth month in a row. Fuel prices, combined with rising housing prices have put CPI to a yearly growth of 2.1% for last year. While oil prices remained relatively flat the past month due to increased shale production, consumer prices may not grow so much in the first quarter. The expectation for this data is an increase of 0.3% but 0.2% for core growth.

Business Inventories (December)

This data represents the monthly changes in inventories from manufacturers, retailers, and wholesalers. This is a key component of GDP. Business inventories are expected to expand strongly for the second month for December. 1.7% is what the gain was for the final quarter of 2016. This was the strongest growth seen in ten quarters. The expectation for December is 0.4% growth.

Retail Sales (January)

Retail sales are expected to have grown 0.1% overall, but 0.4% for auto sales. Auto sales have fallen in recent times, to 0.7% year-over-year for the three months ending in January. Auto sales used to be a large contributing factor to retail sales, but since there are less sales, retail sales have not grown by what they potentially could grow at.

NAHB Housing Market Index (February)

Homebuilder confidence is likely to stay relatively high in February, with this index probably showing a value of 68. There is a strong expectation and belief that future sales will be stronger. January’s data showed that 36,000 new construction jobs were added to America’s workforce, which is the highest seen in 10 months. This would be accommodating for a stronger housing market as new homes will be built.

Euro (EUR)

Spain – Consumer Price Index (January)

Spain’s economy has been outperforming its other EU counterparts. This is why it is likely that there is a 3% year-over-year growth in January’s data. This represents a strong gain from December, which showed a 1.6% year-over-year rise. With a recovering economy in the rest of Europe, a heavy reliance on fossil fuel, and rising food prices, it is likely that there will be a strong inflation pressure developing in coming months.

Euro Zone – External Trade (December)

The trade surplus likely climbed to EUR28 billion from EUR25.9 billion in November, The sudden depreciation of the Euro from the time of the US election supported exports for Euro zone countries collectively. As there is expected to be fiscal expansion in the US, this would ultimately appreciate the Dollar and weaken the Euro at the same time. This will support European exports in the global market since American products will be deemed too expensive at that time.

Great British Pound (GBP)

Unemployment (December)

Unemployment in the UK likely edged up slightly to 4.9% in from 4.8% in November. Even though employment has remained relatively stable from the time of the referendum, some areas have developed cause for concern. Statistics about labor market conditions take time to be reported as they are contingent to fluctuations in the market. Similarly, labor markets are slow to adjust to economic conditions. So, given what the British economy has been going through in recent times, it is likely that unemployment will continue to rise in the coming months, but different industries will be impacted in different ways.